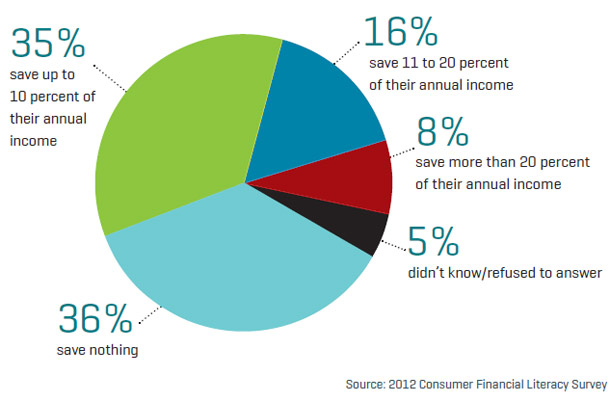

Research has indicated that Americans are making at least modest progress on their savings goals. According to the research, Americans have struggled for years to save adequately for emergencies, retirement and major life events, and that’s still the case. Although only 40% of consumers claim that their progress in meeting savings goals is good or excellent, 70% said they’ve made some progress. Two-thirds are saving a portion of their income, and 63% said they have enough emergency savings to cover unexpected expenses like car repair or a doctor’s visit.

Gavin Gee, director of the Idaho Department of Finance, encourages all Idahoans to take action now to develop or enhance their savings plans.

“In today’s increasingly insecure world, Idahoans can best ensure their financial security by growing their savings,” said Gee. “Having savings allows Idahoans to handle unexpected financial hits, such as a medical emergency or job loss, and to fund some of life’s big purchases, such as a down payment on a home or continuing education, and retirement.”

n the “America Saves” 2015 survey, it was revealed that 73 percent of respondents reported saving their money using traditional bank and credit union savings/checking accounts. The survey also found that more than 60 percent of respondents use an automated method as their primary savings plan. Gee noted, “An automatic savings program is frequently the key to a successful savings plan and our Idaho financial institutions have programs for every saver.”

America Saves Week, sponsored by the Consumer Federation of America and the American Savings Education Council, wants more Americans like Wood to do whatever they can to save. That means paying off consumer debt, building a rainy day fund, saving in a workplace retirement plan and/or an Individual Retirement Account, making savings automatic, and paying down your mortgage.

“It’s important for all of us to better understand the sometimes competing needs of day-to-day living expenses and retirement savings,” says Harry Conaway, chairman of the American Savings Education Council.

“Banks took the money the American people gave them and they used it to pay themselves huge bonuses and lobby the Congress to kill big reform. And then they blamed immigrants and poor people, and this time even teachers.”

On this subdued note, The Big Short closes, having told the story of the reckless banks and Wall Street financial firms and hedge-fund managers who crashed the world economy in 2008. The Oscar-nominated film unpacks sub-prime mortgages, credit default swaps, and other Wall Street-imagined products that swindled American families out of their homes and their retirement savings.

Only about 40% of U.S. households say they’re making good or excellent progress toward achieving their savings goals, about the same percentage as last year. And the number of respondents who are putting away at least 5% of their income ticked down slightly, to 49% from 52% in 2015. Researchers have advised automatically sending a portion of your paycheck directly to your savings account. It’s also worth mentioning that not all seniors have the luxury of working until age 62 or beyond. Our bodies are all different, and our health is completely unpredictable, so to assume that because we’re living longer we can also work longer may be a misguided assumption.

Be the first to comment on "What Americans Are Saving For -It’s Not Retirement !"